|

Brexit diaryOur directors are writing a series of blog posts about the UK public's choice to leave the EU |

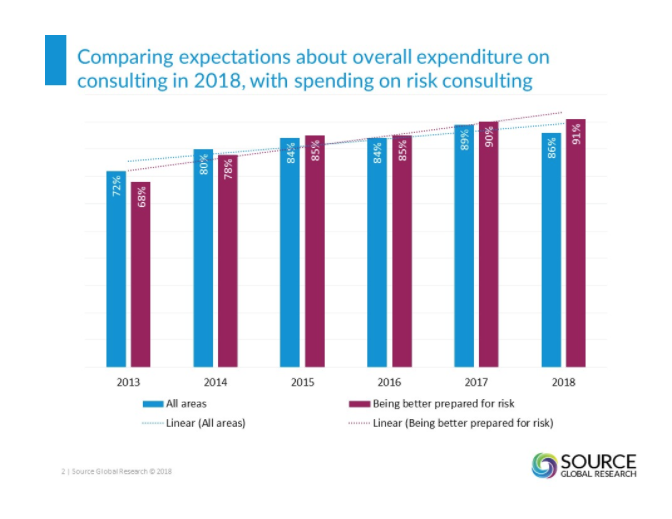

74% to 55%: Two statistics crucial to understanding consulting in 2018Thursday 5th Apr, 2018By Fiona Czerniawska. I’m not always a fan of large-scale thought leadership studies, repeated year in, year out, but the title of PwC’s 21st CEO survey caught my imagination—and, I suspect, the Zeitgeist. In The anxious optimist in the corner office, PwC argues that “despite record levels of short-term optimism in the global economy, CEOs worldwide report heightened levels of anxiety regarding the business, economic, and, particularly, the societal threats confronting their organisations.” Last year, we wrote about what we called the phoney war, the fact that clients were continuing to say they’d spend more on consulting in 2017, despite all the sense of political and macroeconomic uncertainty. A year on, and we see the same signs of mounting anxiety that PwC does. On balance, senior executives are still saying they’ll spend more on consulting, but the proportion who do so has fallen significantly for the first time in the six years we’ve been running this survey, from 74% to 55%. Having doggedly hung on to their investment budgets in 2017, their confidence is ebbing. Even if the economic indicators aren’t markedly different, their cumulative effect is making people nervous. In fact, PwC’s data suggests that uncertain economic growth and its concomitants; changing consumer behaviour; and volatile exchange rates, are less likely to drive anxiety this year, but that cyber threats and terrorism are. The “anxious optimist” is less worried by things going wrong in the business world, and more worried of what could happen in the real world. That, we believe, is going to have an impact on the consulting industry, and we can see early signs of this in our data. Each year we ask around 3,000 senior executives, in large organisations spread across a range of sectors and consulting markets, to tell us what they’ll be focusing on, and investing in, as a business. Aggregate these results together and you get a sense of how busy people will be, and their priorities. Overall, clients expect to be fractionally less busy than they were last year. Don’t get me wrong: They’re still going to be very busy—86% of those we questioned said they’d be making a significant investment in one or more of the areas we asked about—it’s just that that proportion is slightly down on last year’s 89%. But if we compare changes of overall “busy-ness” to the more specific willingness to invest in being prepared for risk, then the latter is rising.

The differences aren’t huge, but—if we were betting people—we’d would put money on the fact that the optimists in the corner office are going to manage their anxiety by spending more on risk consulting. Blog categories: Share this article |

Subscribe to our contentCategories |

Add new comment